Shubham

Tech-enabled home loans for India's emerging consumers

$ 12,000 0

Average mortgage size

$ 825 0 M

Assets under management

200 0

Branches Nationally

Shubham is a specialist affordable mortgage lender that operates in 12 states in India with broad distribution across 200 branches. The company offers loan products to low-income Indian families largely excluded from formal banking services.

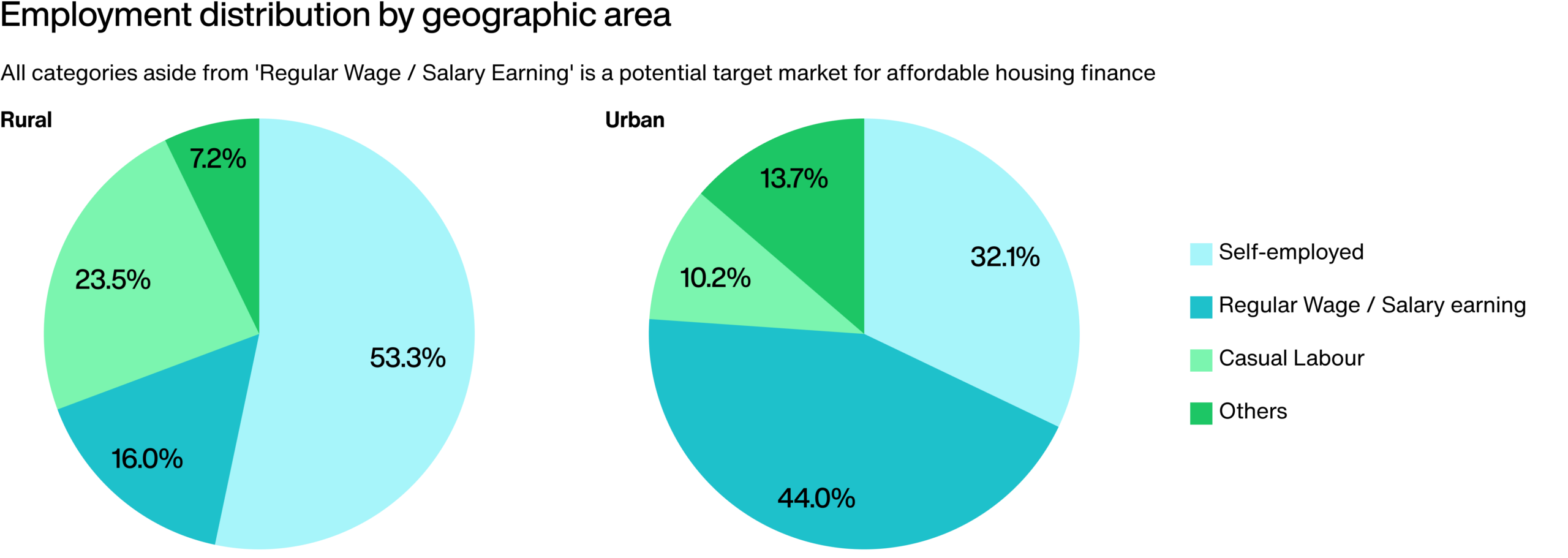

Source: Periodic Labour Force Survey, 2023-24

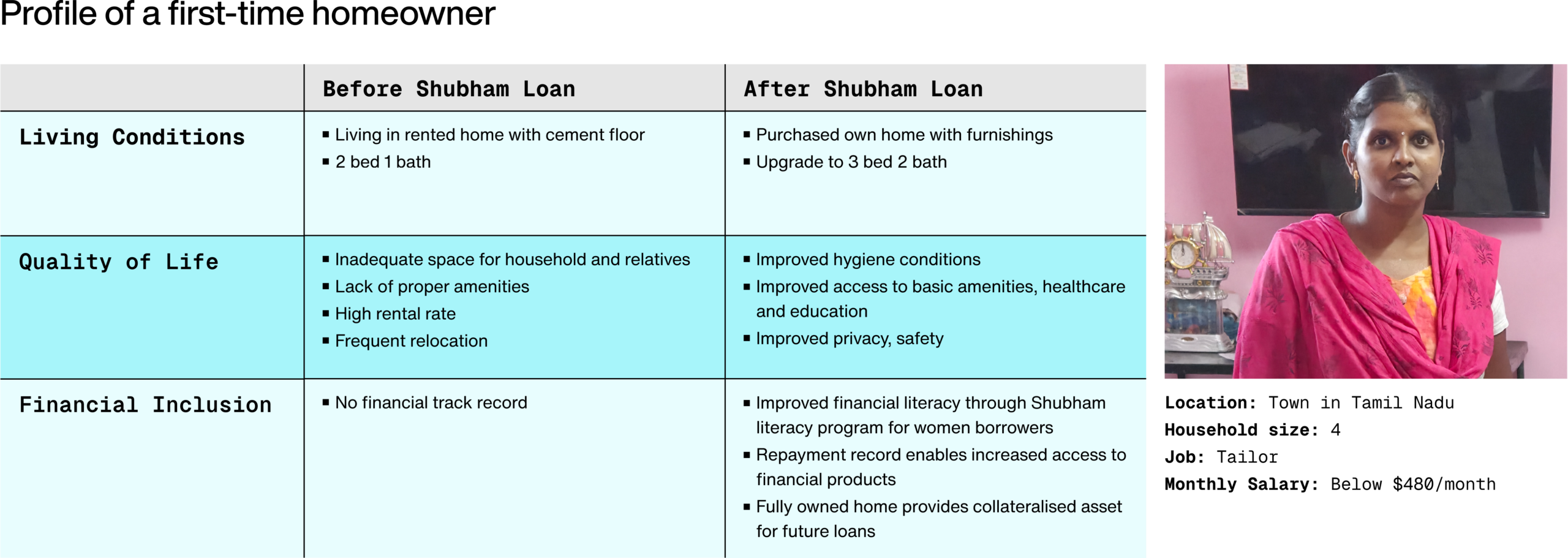

Source: Company Data, 2025